Manufacturing, Indicators, January Effect, Attention, and Super Bowl

Five for Friday - February 7,2025

1. Manufacturing

The U.S. economy has been resilient in the face of higher interest rates almost entirely due to its strong consumer sector (which makes up ~70% of GDP). But just because the aggregate economy has been strong does not mean that every corner of the country is thriving. Take manufacturing. While a much smaller portion of our economy than in the past, it still represents roughly 10% of U.S. GDP and employment. It is also much more interest-rate sensitive, and has struggled with high rates and high inflation in recent years. However, as is usual if we’re writing about it here, there is reason for optimism. Economic activity in the manufacturing sector expanded in January after 26 consecutive months of contraction (per the ISM’s widely-followed survey of supply chain executives), driven by strong levels of new orders, production output, and hiring. Scroll to the ISM survey’s respondent commentary section for boots-on-the-ground reporting. There are still headwinds to a sustained manufacturing rebound (tariffs, rates, etc.), but an uptick here would help provide a nice cushion should U.S. consumption (or government spending) ever begin to meaningfully slow.

2. Inverted

I recently wrote about how yield curve inversion – considered as reliable a recession indicator as there is – got it wrong this time. The message is less about the yield curve itself, and more about how any one single indicator will always struggle to tell the full story of an increasingly interconnected and fast-changing global economy. The allure of the silver bullet indicator is strong (there’s a reason so many charlatans promote their version), but the truth is that no single solution to the investing game exists. It’s a less comfortable position, but the most successful investors are content living in a world of gray.

3. Seasons

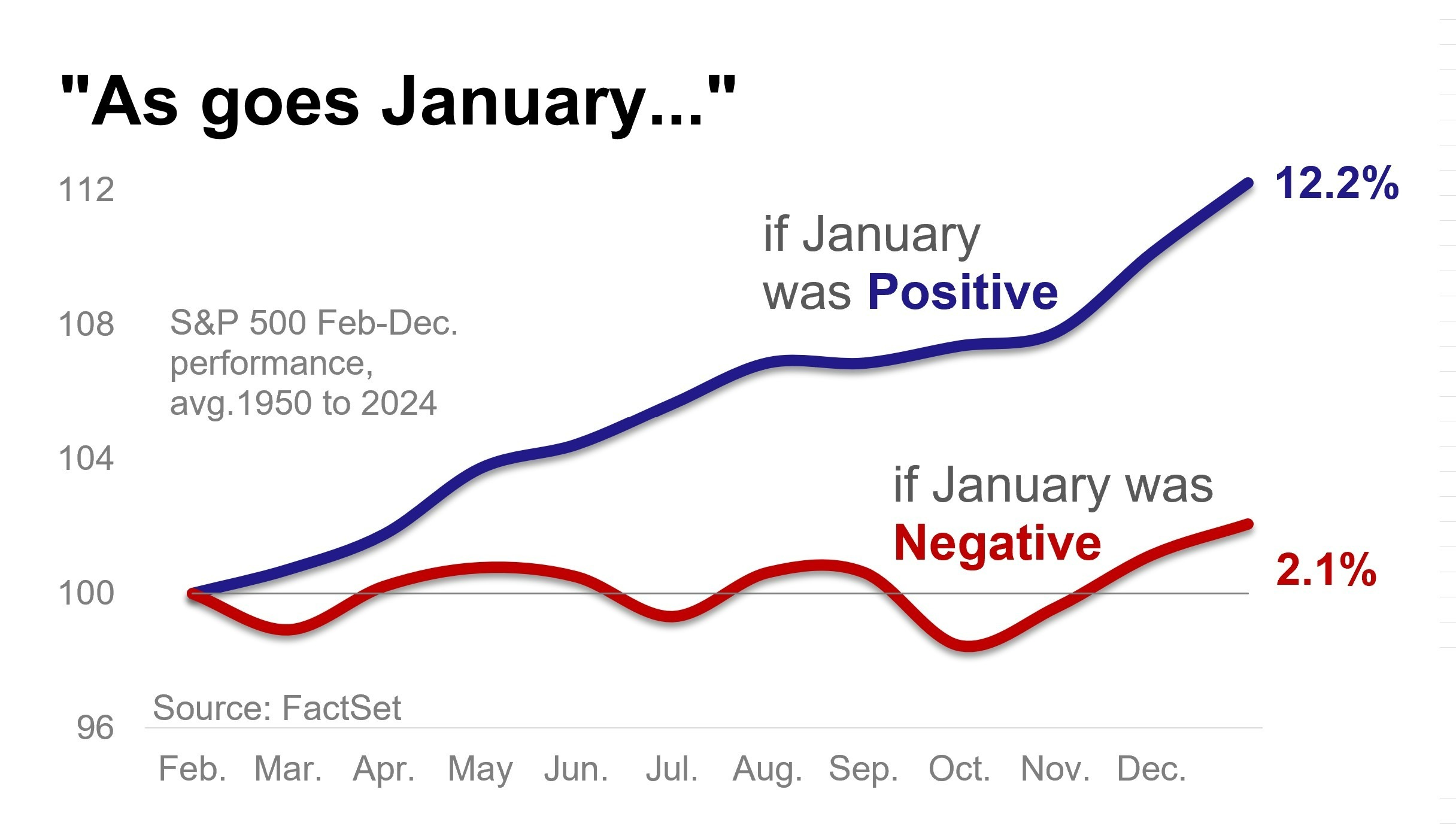

“As goes January, so goes the year.” That Wall Street maxim dates back to the early 1970s but does it hold up to modern analysis? Let’s find out. Over the last 75 years, the S&P 500 has been positive in January 45 times. For those 45 years, the average S&P 500 return from February through December was 12.2% (and was positive 87% of the time). For the 30 negative Januarys, the average return from February to December was just 2.1% (positive just 60% of the time). It’s far from the most important thing investors need to consider, but I’ll take a strong start to the year (the S&P 500 rose 2.7% last month) over the alternative any day.

4. Attention

Matthew Ball’s annual treatise on the state of video gaming includes a chart showing that daily use of TikTok, Facebook, YouTube, and Instagram by U.S. adults has grown from roughly 275 million hours in 2019 to 425 million in 2024. Adults are also increasingly using social media platforms as news outlets. Of course, the great irony of the information age is that digital overload can result in a less-informed consumer and a worse investor. Research has shown that information hyperconsumers often find it harder to retrieve and process relevant information from their available media (i.e., separate “news from noise”), and the increasingly negative and sensationalist tilt of content has a dour impact on both mental health and investing outcomes. Just think of all the “reasons” to sell over the last few years – election volatility, recession predictions, bank failures, geopolitical instability, etc. And at every turn, selling into the uncertainty would have left you poorer as a result. Just because headline volatility is high today does not mean that actionable catalysts must follow. In fact, once your portfolio and plan are created, inaction is often the most powerful action. Remember: what gets attention is rarely valuable.

5. Gambling

Per the American Gaming Association, a record $1.4 billion is expected to be legally wagered on Super Bowl LIX this weekend. Sports gambling has boomed since the Supreme Court overturned a ban in 2018, with revenues at major bookmakers skyrocketing amid a proliferation in consumer access and high profit margin exotic bet usage (e.g., parlays). Keep your eyes here for the latest All That Matters, where Mike and I talk gambling and markets.

Disclosures

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Market and economic statistics, unless otherwise cited, are from data provider FactSet.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should not consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

For investment advice specific to your situation, or for additional information, please contact your Baird Financial Advisor and/or your tax or legal advisor.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Copyright 2025 Robert W. Baird & Co. Incorporated.

Other Disclosures

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W. Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.