Lessons from past disruptions

To help understand how to approach the current moment as an investor, it can be helpful to look at past moments of disruption. In each of the following cases, markets have taken a short-term hit before bouncing back over the long term.

Policy shifts and political volatility

This isn’t the first time tariffs have become front-page news in the U.S. In fact, it happened in 2018, when the first Trump administration imposed tariffs on solar panels, steel and aluminum, among other products. Trading partners retaliated with tariffs of their own, sparking a trade war that contributed to the S&P 500 declining by about 10% for the year. However, the S&P soon bounced back, and by April 2019 it had exceeded its 2018 peak.

Chart 1: Late-208 Trade War Sell-Off

Source: FactSet

Meanwhile, many investors worry that big tax cuts or tax hikes could have major market implications. But while tax changes must be factored into individual financial plans, new tax policies are weakly correlated with S&P 500 performance. This fact remains true whether taxes are changed on an individual or a corporate level, and whether they are being raised or lowered. In short, taxes matter—but not to the markets.

Other examples of political volatility point to the same lesson of long-term market resilience:

- When JFK was assassinated, the Dow Jones immediately fell 3%. However, markets fully recovered within the next two days..1

- During the legal battle over the Bush/Gore election in 2000, markets dropped 8% in just a few weeks before stabilizing and resuming their historical upward trend.2,3

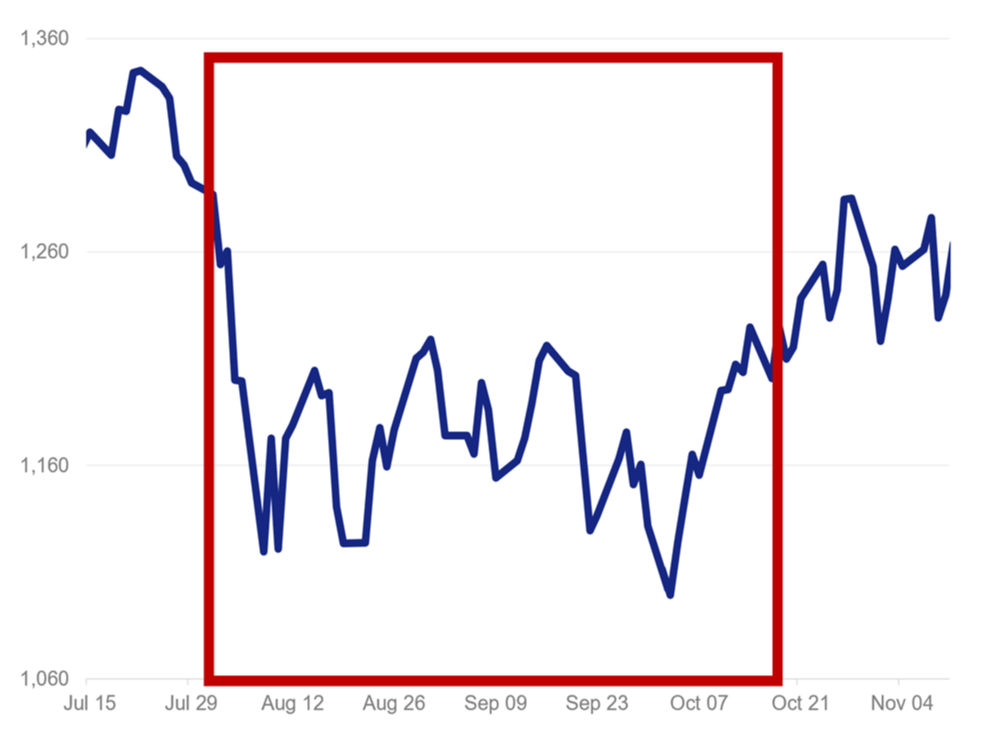

- During the 2011 federal debt ceiling crisis, the S&P 500 fell rapidly at first then retested the market lows before hitting a market bottom several weeks later (and then climbing higher again.4

Chart 2: 2011 Debt Ceiling Crisis Selloff

Source: FactSet

Natural Disasters

Sometimes, disruptions are outside of anyone’s control. Nowhere is this more true than in the case of natural disasters.

So does the relative unpredictability of earthquakes, hurricanes and the like make markets behave any differently than they do in response to human-directed action? Not really. Take these examples from the past 20 years:

- When Hurricane Katrina hit in 2005, the S&P dropped by almost 4% in the storm’s immediate aftermath. It recovered within months.5

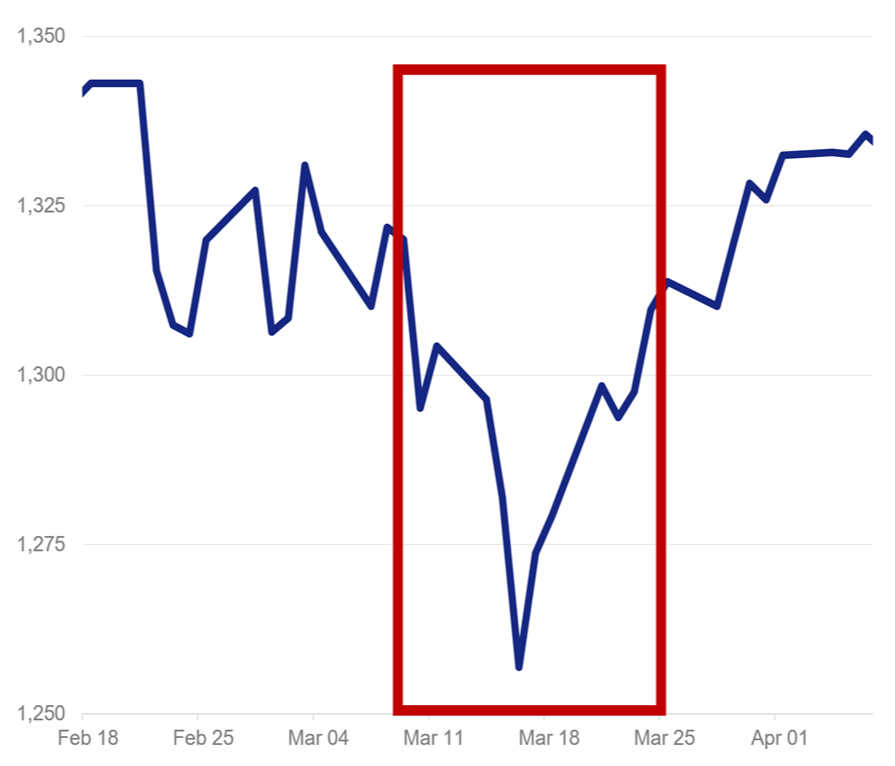

- The 2011 Japanese earthquake and tsunami caused global markets to drop about 2%, as investors feared disruptions in the global supply chain. However, markets soon bounced back.

- Hurricane Sandy shut down Wall Street for two days in 2012. Recovery efforts boosted construction and infrastructure stocks in the following months, and the markets overall were soon churning along on their usual upward course.

Chart 3: Japan Earthquake 2011

Source: FactSet

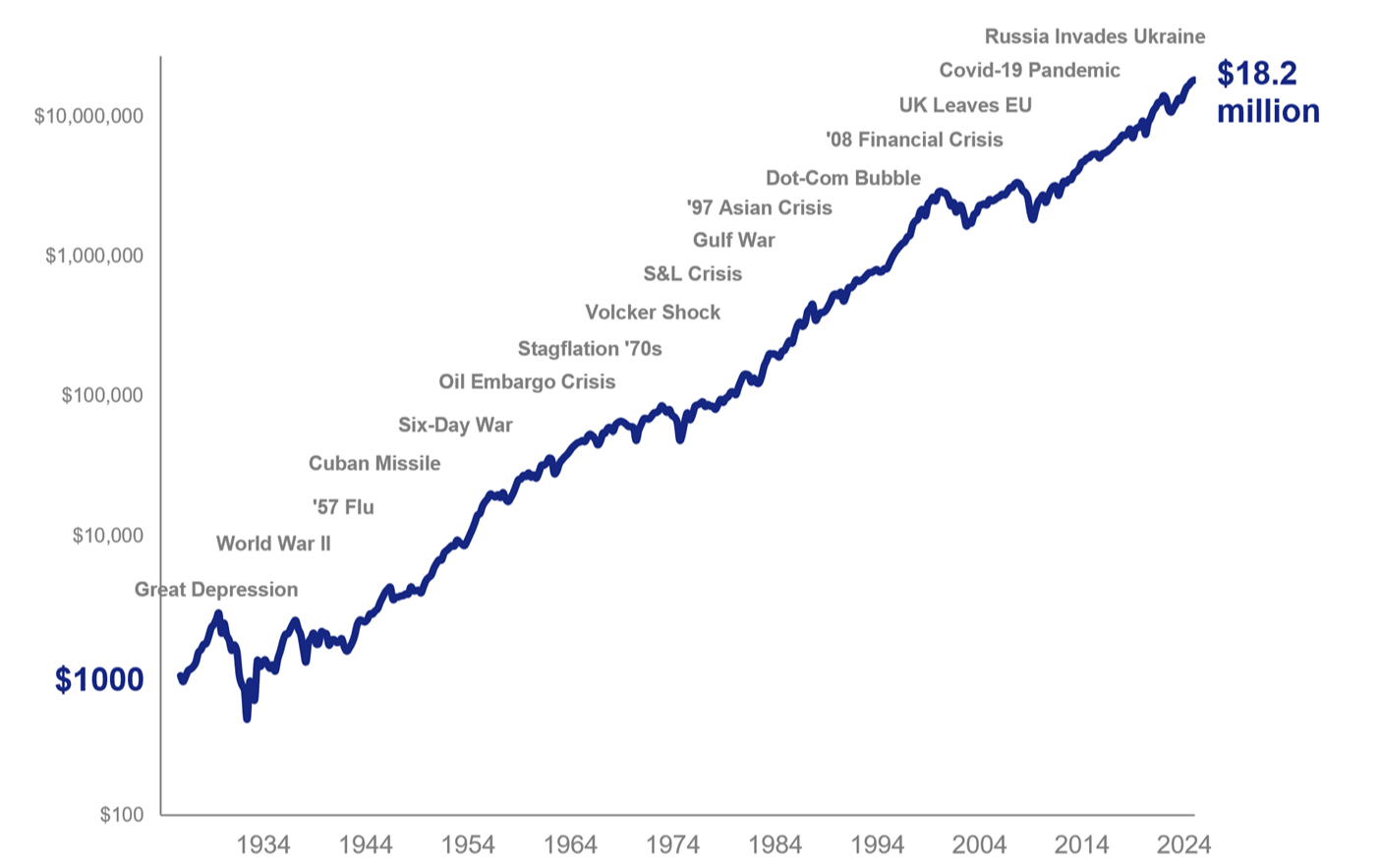

Chart 4: Despite Setbacks, the Market has Recovered

Source: FactSet, Damadoran/NYU, Ibbotson SBBI

The stock market has been hit by countless adverse events over the last century. Some of these took years to recover from while others were minor, now-forgotten blips. But after each of these setbacks, the market recovered and moved on to new highs.

Other Unexpected Events

Some types of disruption fall outside of easy categories and can seem to come out of nowhere. For example, on May 6, 2010, in what would become known as the “Flash Crash,”6 the Dow Jones lost nearly 9% of its value within minutes. At first, no one knew what caused the crash, but later, regulators traced it back to an unusually large sell order instigated by a U.S. mutual fund. Whatever the cause, markets bounced back with the Dow Jones closing just 3% down from where it began the day.

Disruption can come from global competition as well. In January 2025, when the Chinese AI startup DeepSeek unveiled its advanced AI chatbot at a significantly lower cost than other AI systems, shares of many U.S. tech companies tumbled.7 However, most tech stocks began to bounce back within a matter of days.

The list could go on, but the story remains the same: the source of disruption, whether it can be predicted or not, the effect on markets tends to be temporary. For investors, the lesson is clear, says Baird market strategist Michael Antonelli. “What you do during turbulent moments is what matters most for investors,” he says. “Every moment of economic chaos, every moment of policy uncertainty, every time the stock market is sold off based on something happening in the world, what you do at that moment with your money—whether you buy or sell or stay put—is what will have the biggest impact on the long-term results of your investments.”

The reason to hold fast to your plan without buying or selling, Antonelli says, is that what’s happening at the moment on the national and world stage actually has very little to do with what you’re ultimately investing in. “Some people might think they’re investing in what’s going on in the world on a day-to-day basis,” he says. “But what you’re actually invested in, especially in the U.S., is things getting slowly better over time. You’re investing in companies who have workers who created products and solutions. Every now and then, things fall apart. But as long as companies continue to create value over the long term, you’ll be able to participate in their profits.”

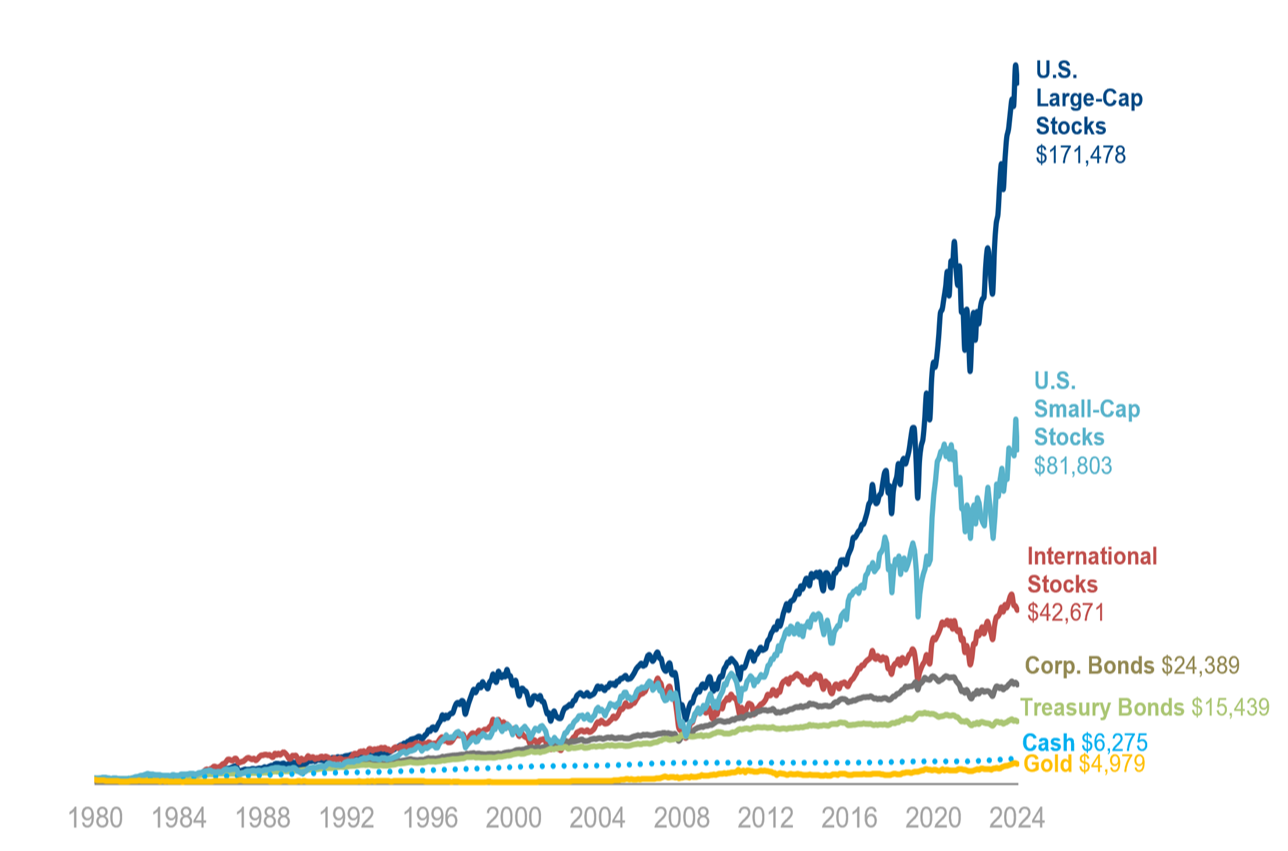

Chart 5: Growth of $1000

Source: FactSet, Damadoran/NYU, Ibbotson SBBI. Asset classes are represented by the following indices: U.S. Large Cap (S&P 500), U.S. Small Cap (Russell 2000), International (MSCI EAFE), Corporate Bonds (Bloomberg US Corp Bond), Treasury Bonds (Bloomberg US Treasury Bond), Cash (Bloomberg 3-mo Treasury Bill), Gold (LBMA $/oz.)

The importance of sticking to your plan

Weathering periods of disruption means letting your investments be guided by a well-considered plan that you create in collaboration with an advisor, rather than making individual investment decisions in response to the day-to-day fate of certain stocks or markets. “There can be dark clouds swirling,” Daley says. “What we go back to is the plan. You can work to undo a bad investment, but its harder to undo a bad plan.”

Here are a few things to do—and to avoid doing—when disruption strikes.

Don’t time the market

Timing the market—while occasionally producing short-term outperformance—almost inevitably leads to underperformance compared to the market overall. Yet the temptation to avoid big losses or gamble on big gains can be so strong for investors that it often leads their investments to underperform major indexes. For example, in 2024 alone, the average investor saw an annualized return of 16.5%, while the S&P 500 saw an annualized return of 25%.8

“We always discourage investors to try to time the market, because it’s virtually impossible,” Daley says. “Sometimes you get lucky, but most of the time you don’t.”

Diversify

For many investors, seeing markets plummet in the space of hours or days can be a shock to the system—even if they know that markets generally recover over the long run. But while it’s hard to avoid the negative impact of plunging markets entirely, that impact may be mitigated by a diversified portfolio. This effect is due to the well-documented fact that different asset classes perform well at different times. To take a classic example, bond markets tend to have a negative correlation to stocks, meaning they often rise when stocks fall, which is why most investors typically have at least some exposure to bonds.

Diversification can happen on a more granular level as well. For example, growth stocks (shares of companies with high potential for future earnings) and value stocks (shares of companies that appear to be undervalued by the market) often move along separate trajectories. Likewise, U.S. stocks aren’t always correlated with international stocks.

Chart 6: Importance of Diversification

Source: FactSet. Large Growth is represented by Russell 1000® Growth Index. Large Value is represented by Russell 1000® Value Index. Mid Cap is represented by Russell Midcap® Index. Small Cap is represented by Russell 2000® Index. Taxable bonds is represented by BBgBarc. Agg. Bond Index. Municipal bonds is represented by the BBgBarc. Municipal Index. International is represented by The MSCI EAFE Index. Cash is represented by FTSE Treasury Bill 3 Mon.). Commodities are represented by the Bloomberg Commodity Index. Indices are unmanaged and are used to measure and report performance of various sectors of the market. Past performance is no guarantee of future results and diversification does not ensure against loss. Direct investment in indices is not available. The Russell Indices are a trademark of the Frank Russell Company. Russell® is a trademark of the Frank Russell Company.

“For the last decade or so, growth has pretty handily outperformed value, and domestic stocks have outperformed international stocks,” Daley says. “What we’re seeing so far in 2025 is the exact reverse of that. These days our global and value funds have really been propping up our growth portfolios. It just proves that there’s good reason to hold value and international stocks in your portfolio.”

Rebalance

Sticking to your financial plan doesn’t necessarily mean not making any adjustments to it. Rebalancing your portfolio in collaboration with your advisor can help you work toward long-term investment goals while striving to reduce risk. That’s because some types of investments may grow faster than others, leading to imbalances in your portfolio relative to your target allocation. Here, again, the principle that different assets move along different trajectories is key.

“At the end of 2024 we helped a lot of clients rebalance in one of two ways,” Daley says. “First, if people were getting a little short on their bonds, we pared back the equity exposure and added it to their bonds. And second, we harvested gains from growth stocks and moved some of it into value stocks, which is paying dividends now as growth takes a hit.”