Loss Aversion and Recency Bias

Understanding two common behavioral biases:

What’s behind the financial decisions we make? Often, these decisions are the product of behavioral biases shared by most people. Understanding these biases, however, can help investors more easily spot them and keep them from knocking their plans off track. Here are a two of the most common biases: Loss aversion is the tendency for the potential of a loss to feel more painful than the potential for a gain. For investors, loss aversion may lead them to adopt a more conversative approach than is appropriate. Recency bias is the tendency for investors to be strongly influenced by the latest news reports or market movements. However, making long-term financial decisions based on recent headlines can lead investors to chase hot stocks or sell in the wake of an unexpected market downturn.

One of the most common investor biases is loss aversion—the tendency of investors to fear losses more acutely than they anticipate the prospect of gains. As Ashcroft points out, loss aversion is a natural reaction. “If a client is upset by seeing losses in their portfolio, that’s the reaction I would hope they’d have,” he says. “If they weren’t upset, I would be concerned about whether or not they were really understanding what was in front of them.”

The problem arises when investors put too much weight on their fear of losses. It may lead investors to panic and sell when markets dip or adopt an overly conservative approach that limits the potential for losses—and the potential for growth.

Another common investor bias is recency bias. This is the tendency for recent events to have an outsized influence on investors, causing them to make ill-advised short-term changes to their long-term strategies. “Things that happened recently are going to be top of mind for basically anybody,” Ashcroft says. “It’s just how we work as human beings.”

The recency bias could manifest in the form of investors throwing all of their money on a few stocks that have outperformed over the past few months, for example. And it could be exacerbated by the herd mentality bias, the tendency for investors to follow the path of other investors, even if that path isn’t rational. If a group of stocks has been doing well lately, and a significant portion of investors overinvest in those stocks, the recency bias and the herd mentality bias could work together to drive investors to follow the money. Over the past couple of years, for example, investors have swarmed to the so-called “Magnificent Seven” tech stocks, which have been riding a hot streak. The problem is, today’s outperforming stocks can be tomorrow’s laggards. For investors that jumped in when prices were high, a reversal of fortune for a once high-flying stock can leave them in the lurch.

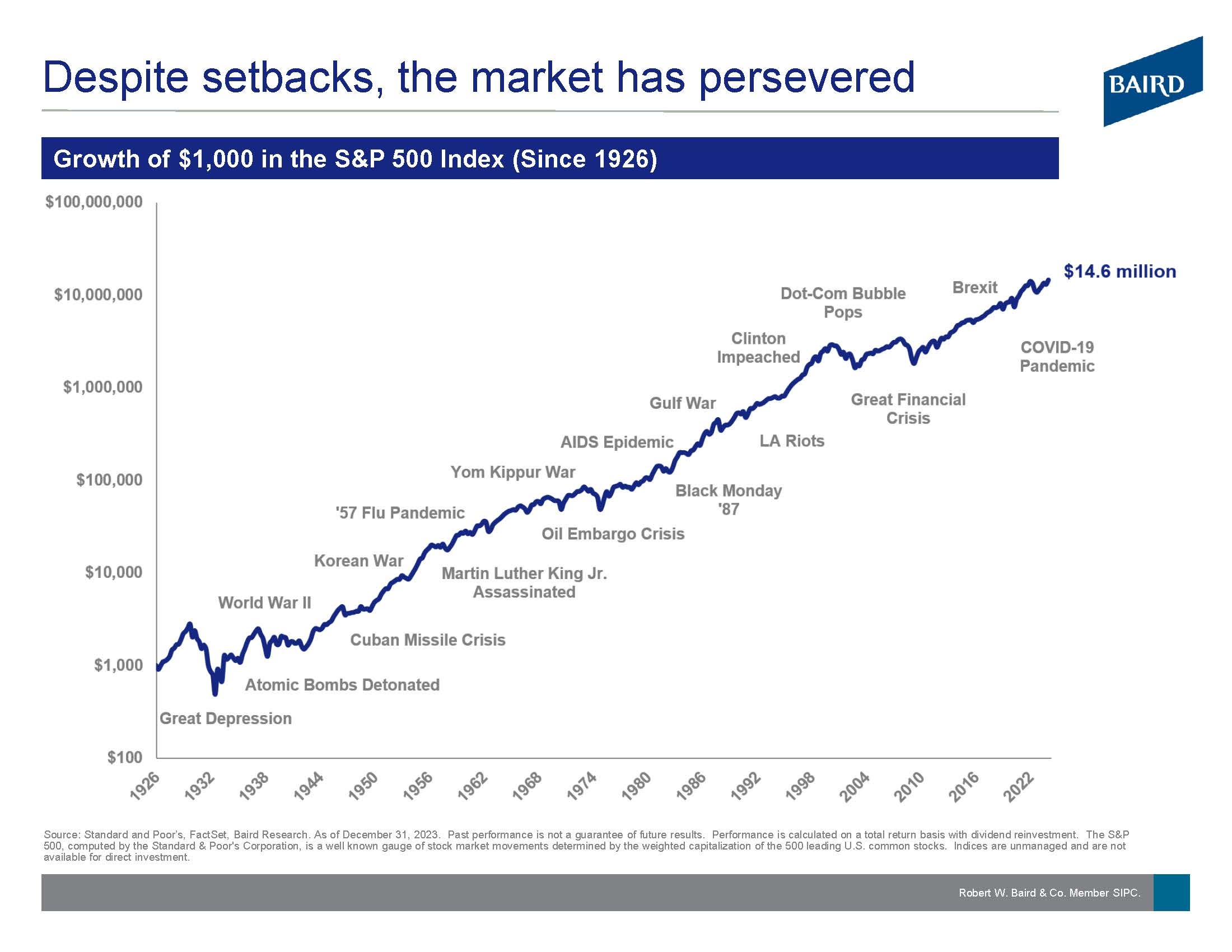

Investors aren’t wrong to have these sorts of biases. They’re a product of human evolution, hard-wired into our brains to protect us from real threats. If a tiger raided a village one night, there was a decent chance that it was still in the area and would be back the following night, and it made sense for villagers to be on guard. But the stock market isn’t a tiger, and short-term investing losses tend to transform into significant gains over time. “Our hardware is not well suited for the environment in which we find ourselves,” Ashcroft says.

The point, then, isn’t to get rid of our biases. It’s to become familiar with them and make peace with them. Gaining a better understanding of what drives our decision making can help investors rein in their impulses to take unwarranted action in times of uncertainty.